ICBC (Industrial and Commercial Bank of China) Personal Pledged Loan

Written at: 02 Oct, 2025

You’re likely curious about how their loans work, what are their charge, or how long they take to respond. And you were searching online when you found this article. Unfortunately, it doesn’t work that way, as explained here. While MAS introduced the Guidelines on Standards of Conduct for Digital Advertising Activities in September, they’re still not extensive enough. Unlike in the UK, where an advertised 1% or 1-hour loan must apply to at least 51% of borrowers, that’s still not the case here. More worrying are the intermediaries not owned by banks but generating leads for them. And this is why you need to read this article.

Personal Pledged Loan - by the way, probably means you need to be a guarantor to the loan, and they can sue you for nonpayment, like all other banks. It could mean it needs to be secured, though not much information can be found on ICBC's website. And this is what we are trying to tell you with this "review."

As we have seen so many “comparison” portals or bloggers reviewing it, we thought we would chip in, but with a twist. Telling you how many so-called review or loan comparison websites actually work.

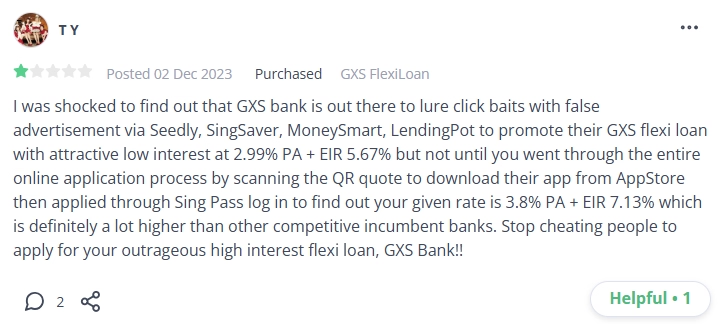

Credit: Public review found on Seedly and Google

Not all comparison portals are what they claim to be—many are nothing more than paid advertising platforms, serving the advertisers that pay them.

Across markets from the U.S. to Australia, regulators are discovering that these platforms often highlight results based on payment, not on what’s truly best for the borrower or consumer. What you see isn’t always an unbiased comparison but a curated list bought by those who pay the most. And thus we built FindTheLoan.com, Singapore’s 1st loan marketplace. Instead of teaser rates or applying with multiple lenders one by one, you can reach multiple lenders at once with your actual documents, and they will make a full credit assessment as if you had walked in to them individually, and they will revert with their actual offer.

While general information, such as miles or points per dollar spent, is easy to research, loan amounts and interest rates are highly personal. They change from one borrower to another based on each individual’s credit score & profile. That rate they “reviewed” or “compared” for you is actually a teaser rate. Here’s how it works in detail. They are rates that you may or may not get, and in many countries, regulators are either suing them for clickbaiting consumers or publishing warnings on them.

But if you are pressed for time, you don’t have to read the article above - here is an image that tells you everything you need to know about such sites.

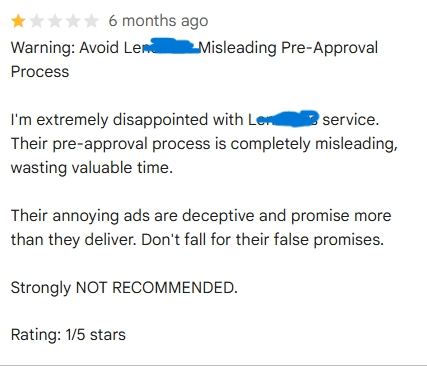

Credit: Head of Lendingpot. Strangely enough, Lendingpot appears to be exposing its own practices. For more of their contradiction or to join the conversation, click here. Even more striking—after we pointed out the conflict of interest in brokers owned by lenders, they parroted the same claim months later. This, despite being owned by IFS Capital & PhilipCapital! Perhaps they’ve simply been copying our work without realizing the mistakes it creates for them?

Every now and then, you’ll see them write comparisons like “this loan vs. that loan.” But think about it—if they claim to compare 10 loans, did they really take all 10 and pay interest on each one?

MoneySmart says it attracts 60 million visitors across Southeast Asia — a reach many lenders and investors continue to amplify despite such platforms' track record of misleading ads. We can’t stop their funding, but we can call it out together. Because this pattern isn’t unique — it’s part of a broader trend we’ve seen across several loan-matching sites, including Lendela, Roshi, Lendingpot, and SingSaver.

"The world will not be destroyed by those who do evil, but by those who watch them without doing anything", Albert Einstein

So we invite you to share your thoughts on this LinkedIn post or on our Reddit, TikTok, or Facebook post, if you prefer. However, we have tagged quite a number of members of parliament on LinkedIn who, during parliament, have asked about matters such as greater consumer protections. Weighing in there, and as more people share their thoughts there, could finally catch their attention to do something about the industry and better protect borrowers. Every comment, repost, or show of support matters — it increases the chances that policymakers take notice and act.

If you enjoyed this article, we’d love for you to share it with others who might find it valuable. Even a quick like or comment here helps trigger the algorithm to reach more people! Our goal is to bring you insights that Big Finance doesn't want you to know, but they often get overshadowed by Big Finance's content due to the large budget they have. Every share helps amplify our work and reach more readers like you!

Subscribe to our LinkedIn newsletter here or on Medium here and never miss any new articles!

Explore next: Loan Brokers: 10 Insider Tips Every SME or borrower Should Know

Give us a try — it’s free to get your personalized loan offers today!

Ask ChatGPT or Perplexity about this.

Share on: